As we limp into the end of the first half of 2022, we’ve witnessed one of the worst yearly starts in the markets since 1962. With a decline of about 20 percent in the S&P 500, 25 percent in the small-cap index, and 30 percent in the Nasdaq, it makes this year the third worst start in market history.

Stocks are now firmly in bear market territory but that is a fraction of the pain being felt in stocks and other risky assets. Stocks are now down 11 of the last 12 weeks but the pain was concentrated in June.

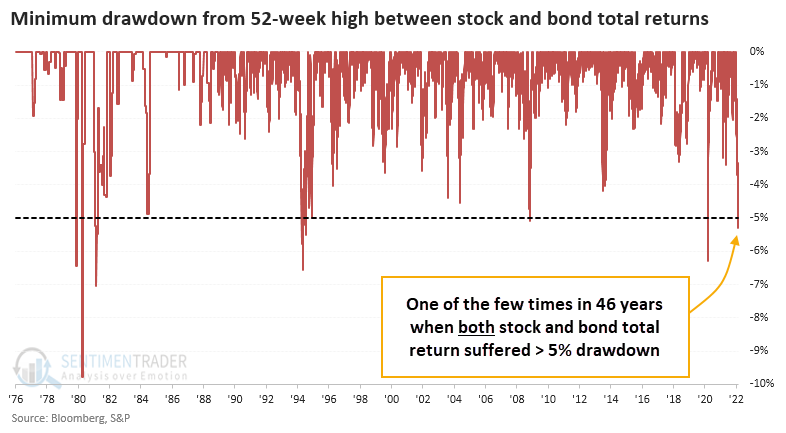

Adding insult to injury, this has also been one of the worst starts for the bond markets in more than 40 years. Long used to add ballast to portfolios as a haven from the stock market storms, the Barclays Aggregate Bond Index is down 10 percent year-to-date, with long-term treasuries down more than 20 percent. Even short-term treasury notes are down almost four percent, making even the safest and shortest of duration government bonds not immune from the carnage. Of course, when bond prices decline, their yields increase, so they become more attractive for new investments. Savers will finally get some return on capital.

Mid-term election years have historically been lackluster for markets, but that doesn’t entirely explain why this year has been so awful. The same issues we've been talking about this year remain front and center:

The war in the Ukraine

Rising inflation

Higher interest rates

The Fed draining liquidity out of the system

You can add recession risk, which seems to be front page financial news on a daily basis. A resolution to any of these issues would go a long way to releasing the selling pressure overhanging the markets.

To OAM's credit, we were very concerned in 2021 with the excesses we saw taking place. I have worked in the financial industry since 1987 and have seen all kinds of market environments. The crypto/NFT/SPAC/meme stock craze of the last few years was truly stunning and I think easily surpassed the excesses of the dot com era. That led us to bring risk levels below target, and hold higher allocations in cash and cash-like investments than ever before. While it's never pleasant to experience any drawdown, it did certainly mitigate the damage.

A question I'm getting asked a lot is, where is the money from all this selling going? How can everything go down at once? It's not going anywhere. It's telling us that the era of zero percent interest rates is over.

Zero rates allowed corporations to borrow money and buy back their own stock. It allowed hedge funds and investment banks the chance to lever up their books at minimal cost. For example, the U.S. 10-year treasury bond has yielded a miniscule 1.5 percent for the past few years. But if you can borrow at zero percent and then leverage up 10x or 20x, you're talking real money. Those types of trades are now gone, and are either being unwound by choice or by margin calls. That's also why the selling has been so consistent and unrelenting across all markets.

So what does that mean for the second half of the year? We know the US economy – the global economy – is slowing. That isn’t news anymore. But I'm seeing it being presented as if a recession is a forgone conclusion. That I'm not so sure about. Banks, which were clearly the biggest source of concern in 2008, are in much better shape than they were then. Right now, anyone who wants a job can get one. And while I'm having a lot of conversations regarding recession, no one I'm talking to is being impacted by the slowdown. To the contrary, business-owner clients are full-out, and everyone seems to be taking vacations.

With so many moving parts, I don't expect things to be resolved right away, so expect a bumpy ride for a bit. We are still about 10 percent higher than we were right before Covid hit, and back then we had low inflation, cheap oil, functioning supply chains, and easy money policies.

On the plus side, the vast majority of the fall in stocks this year had nothing to do with fears of a slowing economy. In fact, the drop was much more about the rise in interest rates which was driven by inflation fears. Now inflation fears are fading rapidly as commodity prices drop. This is also being confirmed by interest rates moving lower, a positive sign.

Historically, of the 14 other worst yearly starts since 1931, 10 of them went on to turn in positive returns for the second half of the year, although only 5 of those 14 years turned things around and closed with positive returns for the entire year.

Lastly, here's an updated chart from J.P. Morgan that I've shared over the years. Stocks and bonds have positive returns over time, but on a year-by-year basis, especially with stocks, it is an almost 50-50 chance that they will be up or down. This is normal market behavior, and this uncertainty is the reason stocks return so much more than bonds over time.